Renters

Apr 29, 2021

How to rent an apartment without a security deposit

Larenz Brown

If you’re reading this, you’ve probably paid a security deposit before. Traditional security deposits require renters to provide a lump sum of cash to their property just to be able to move in. What that means is you’re essentially giving your property a loan for damage that may or may not happen. If that seems backwards to you, that’s because it is.

Security deposits also create questions for renters about if what they’re paying is a typical deposit amount. It can also be difficult to understand the security deposit refund process.

The good news is you can avoid these questions by avoiding security deposits. What was once a mandatory requirement is now a transaction where renters have options.

How do security deposits work?

Step-by-step:

You pay your security deposit

Your property puts the money in a bank account called an escrow account. It is illegal for your property to touch your money while it sits in that account

When you move out, someone from your property will inspect your unit and decide if money will be deducted from your deposit to pay for damages before it’s returned to you.

How to avoid paying a security deposit

In a survey conducted by Rhino, 79% of renters reported that the ability to pay lower upfront fees was an important part of their decision to move. Renters across the country are calling into question the outdated traditional deposit process, resulting in many properties exploring solutions that allow renters to satisfy their security deposit requirement without paying a lump sum up front. These solutions are known as “security deposit alternatives,” and they all use a form of insurance to replace security deposits and keep property owners protected just like a normal deposit would.

What is a security deposit alternative?

Security deposit alternatives make it more affordable for renters to move into a new home. Instead of paying a deposit to a property owner, you’ll pay one of these deposit alternative companies a small fee and they’ll provide your unit with the same protection as a deposit for your entire lease. If you choose the right company, you’ll pay a fraction of what you would’ve with a security deposit. Types of deposit alternatives include:

Lease insurance products

Guarantor products

Credit authorization products

Bond products

Different types of security deposit alternatives

The difference between deposit alternatives really comes down to how they structure their insurance. There’s lease insurance, which is a bit more expensive for renters and lets property owners collect an added fee to rent instead of a cash deposit. Companies like Leaselock use lease insurance to simplify the process for owners at the expense of transparency and affordability for renters.

There are also deposit alternatives specifically designed for renters who need guarantor coverage. These products are typically the most expensive and are offered by companies like The Guarantors.

Credit authorization products hard-wire your bank account to your property owner’s so they can make automatic deductions in the case of damages. These alternatives prioritize convenience for owners at the expense of privacy and due process for renters in the case of damages to the apartment. They’re offered by companies like Obligo.

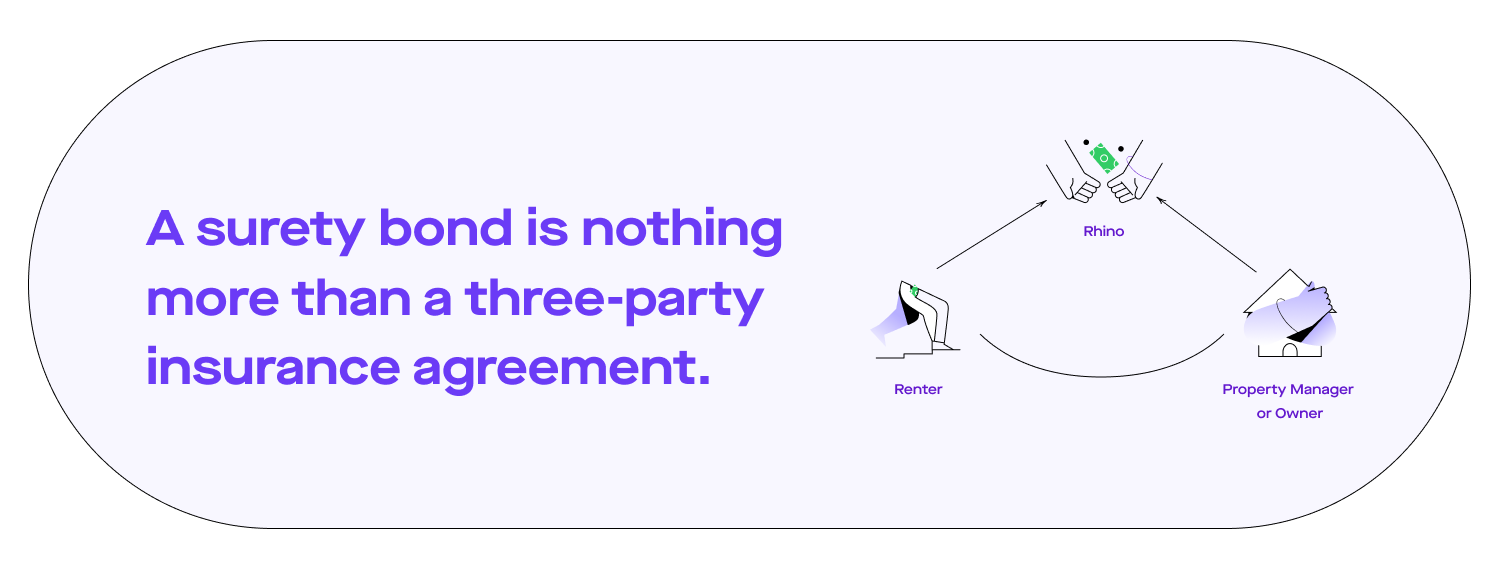

There are also bond products (which is what we are!) that come in all shapes and sizes. What’s common between them is that they use a surety bond to deliver their insurance to renters. A surety bond is nothing more than a three-party insurance agreement, and not all surety bonds work the same.

Security deposit insurance gives renters the best deal

We’ll try to tell you the facts without sounding too biased. Security deposit insurance is how Rhino creates win-wins for renters and property owners. If you do the math for a renter trying to replace a $1,000 deposit, most cases result in Rhino offering the lowest price (between $5 and 13/mo. on average.) Renters can also choose to pay monthly or in full when they purchase the insurance at move-in.

Renters call the shots now. If you play your cards right, you can avoid traditional cash deposits completely and let a deposit alternative do all the hard work for you. You’ll be faced with many choices, but security deposit insurance is the only deposit alternative that prioritizes transparency and affordability for renters.

Visit the Rhino homepage to learn more about security deposit insurance.

Larenz Brown

Larenz Brown is a copywriter at Rhino who wants to tell stories that empower people. He once engaged in a 365-day staredown with a security deposit and emerged victorious.