Renters

Jul 07, 2021

How much should you spend on rent?

Larenz Brown

Looking for a new apartment? When apartment hunting, you may feel pressure to spend big on a good location and all the amenities you want, especially when you feel financially secure. Before you start your apartment search, it is crucial to understand how much you can actually afford to spend on rent and how to budget, considering your annual salary and existing expenses. Afterall, the ideal apartment is one that isn’t going to break the bank.

The 30% rule

While every financial situation is unique, spending approximately 30% of your gross monthly income on rent is a general rule of thumb. By no means is this a hard-and-fast guideline, but if you search for apartments with rent that comes close to this figure, you should be able to secure a relatively comfortable living situation. You will also have enough money for the rest of your essentials and future financial goals.

For example, if your monthly income is $4,000 before taxes, you should look for apartments with a monthly rent of around $1,200. Again, keep in mind you may find monthly rents much higher or lower than what this rule recommends, depending on your city.

In an especially affordable area, you might be able to find an excellent apartment for significantly less than 30% of your income; conversely, in a big city that has a higher cost of living, like New York City or San Francisco, you might not be able to avoid spending half of your income or more on rent. (Be on the lookout for rent concessions and no-fee apartments to help lower the price of rent in these major urban areas.)

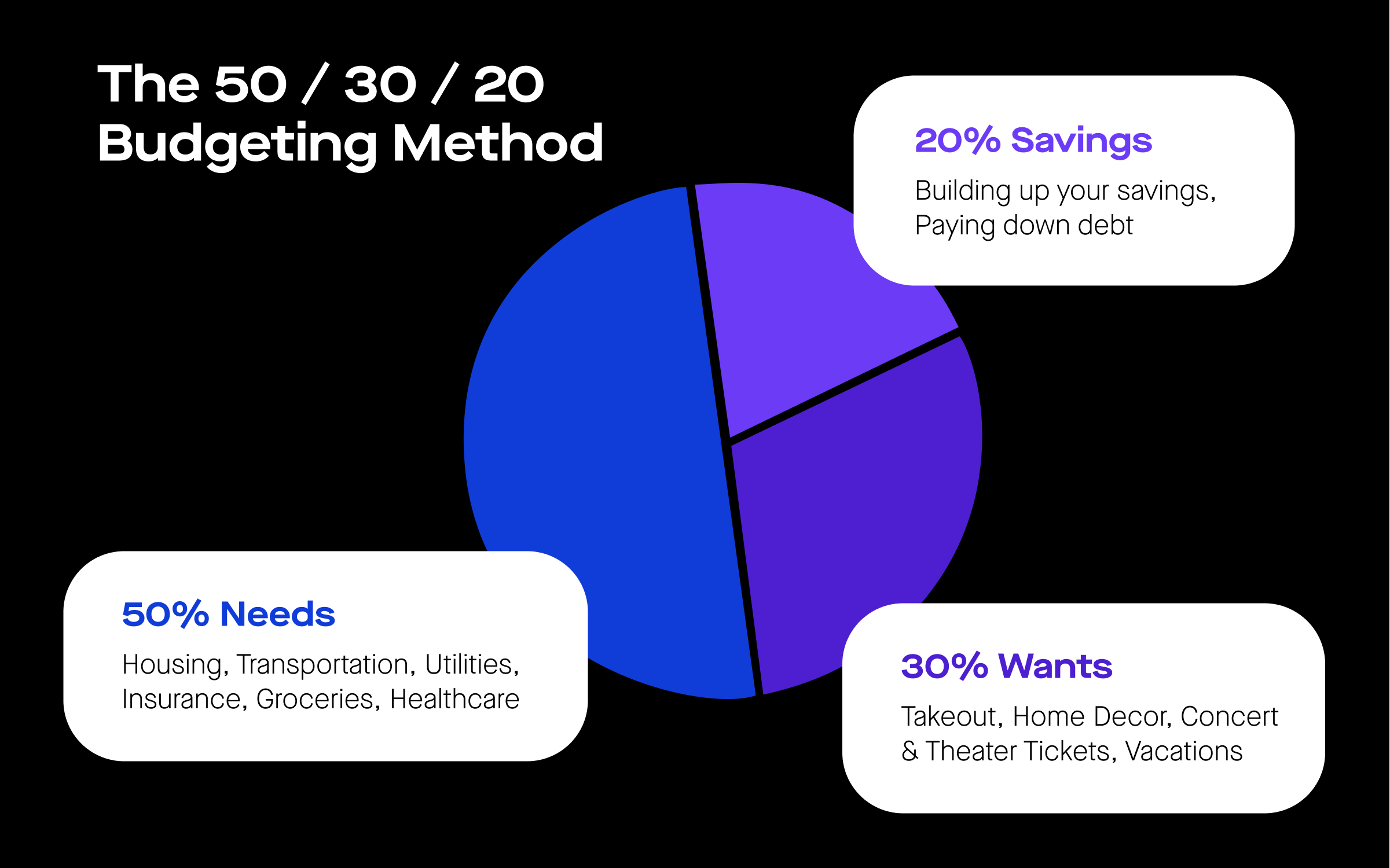

Budgeting with the 50/30/20 rule

A convenient budgeting method is the 50/30/20 rule, which splits up your monthly income into percentages, each accounting for different monthly expenses.

50% — Under this guideline, you should plan on spending around 50% of your monthly income after taxes on your needs, such as:

rent

insurance (including health, car, and renters insurance)

student loans

groceries

utilities

any credit card debt payments

Because you have to make sure you budget enough for these costs, if you routinely spend over 50% of your take-home pay here, it might be necessary to adjust how much you spend on other, non-essential aspects of your life.

30% — After your needs are taken care of, this method recommends budgeting 30% for your wants. Wants may include:

a new phone

eating dinner out at a restaurant

a vacation

These costs can fluctuate from month to month, so it is important to keep a keen eye on how you are spending your money. If you accidentally overspend one month, you will likely have to dial it back in the future to maintain your monthly budget.

20% — The remaining 20% of your monthly income should be set aside for:

savings

investments

retirement

Allocating money each month for an emergency fund can come in handy when you encounter an unexpected expense, such as your car breaking down, or you lose your job. A three-month emergency fund to cover your living expenses is encouraged, and once you are able, replenishing this fund is crucial.

Once you have established that, the rest can be directed towards retirement savings and other financial goals. Saving money can come in different forms. You might be content keeping money in a bank account, or you can invest in a mutual fund or the stock market.

By following the 50/30/20 method, on a $4,000 monthly income level after taxes, you should aim to spend $2,000 on your needs, $1,200 on your wants, and save $800.

Other expenses to consider

Every city is different when it comes to considering housing costs that you will have to factor into your budget:

An apartment located further away from the city center is typically cheaper and thereby lowers your cost of living, but could make getting to work a hassle.

If you take public transportation to work, you could spend extra money per month for rent.

Different homes in different regions can mean drastically different utility costs, so finding a landlord where some utilities are covered in your rent payment can be a huge help.

And when you’re looking at your personal finance plan, look to save money wherever possible:

Instead of budgeting a monthly fee to visit a gym, check to see if your apartment complex has a fitness center.

Plan your weekly meals in advance to cut down on excess food spending.

Utilize coupons to aid in affordability of everyday items.

Understanding these financial factors is an important part of planning your monthly budget.

It all boils down to keeping a budget, saving where you can, and reaching your goals! Take the time to notice and train your financial habits so that your money starts working for you, and work towards reaching a comfortable balance between what you need, what you want, and being prepared for the future.

Fiscal responsibility can be difficult, but it is pivotal to be aware of precisely how you are spending your annual income. Rhino makes renting (especially moving) more affordable which will give you extra cash when you need it. Get a quote today.

Larenz Brown

Larenz Brown is a copywriter at Rhino who wants to tell stories that empower people. He once engaged in a 365-day staredown with a security deposit and emerged victorious.